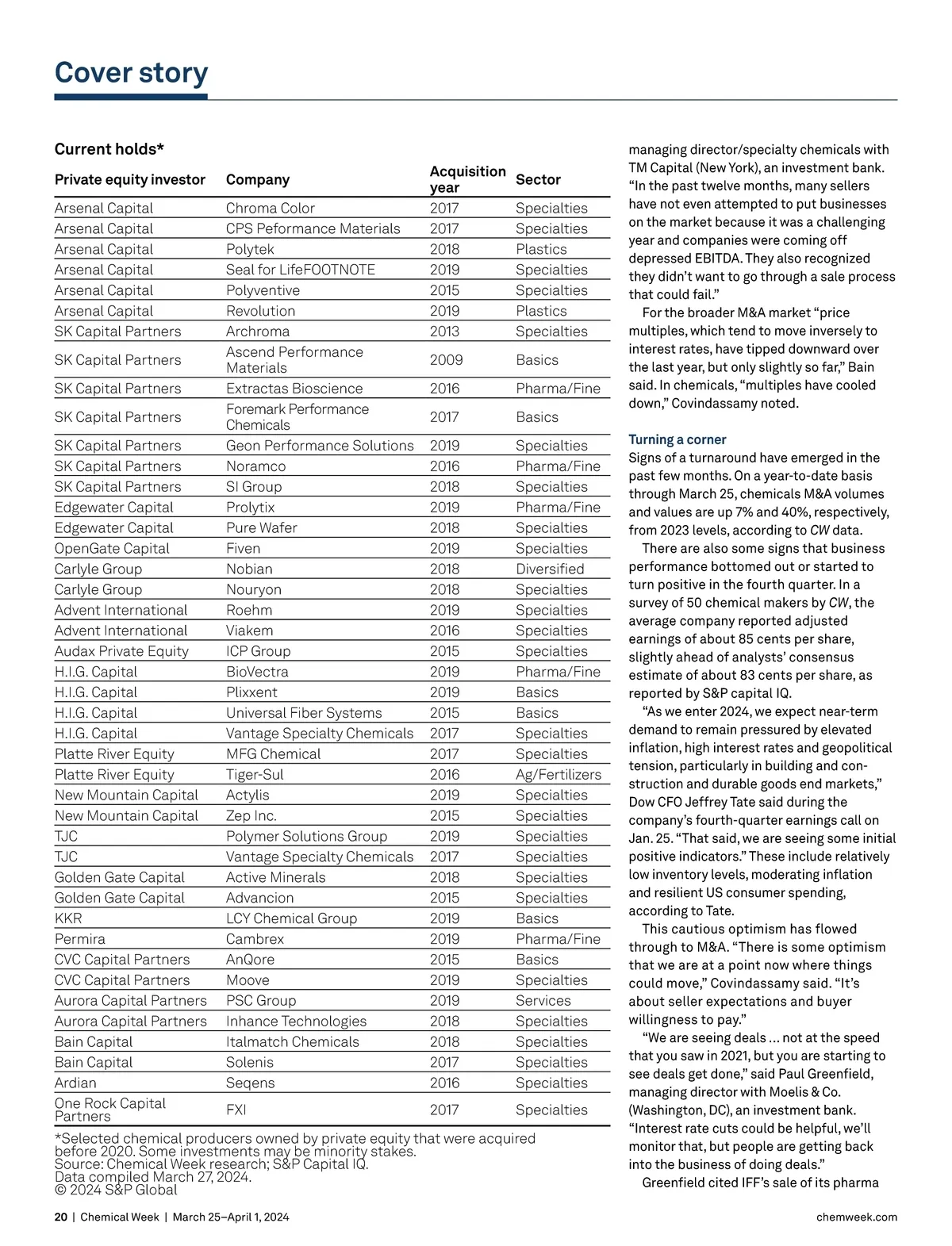

Cover story Current holds* Private equity investor Arsenal Capital Arsenal Capital Arsenal Capital Arsenal Capital Arsenal Capital Arsenal Capital SK Capital Partners SK Capital Partners SK Capital Partners SK Capital Partners SK Capital Partners SK Capital Partners SK Capital Partners Edgewater Capital Edgewater Capital OpenGate Capital Carlyle Group Carlyle Group Advent International Advent International Audax Private Equity H.I.G. Capital H.I.G. Capital H.I.G. Capital H.I.G. Capital Platte River Equity Platte River Equity New Mountain Capital New Mountain Capital TJC TJC Golden Gate Capital Golden Gate Capital KKR Permira CVC Capital Partners CVC Capital Partners Aurora Capital Partners Aurora Capital Partners Bain Capital Bain Capital Ardian One Rock Capital Partners Company Chroma Color CPS Peformance Materials Polytek Seal for LifeFOOTNOTE Polyventive Revolution Archroma Ascend Performance Materials Extractas Bioscience Foremark Performance Chemicals Geon Performance Solutions Noramco SI Group Prolytix Pure Wafer Fiven Nobian Nouryon Roehm Viakem ICP Group BioVectra Plixxent Universal Fiber Systems Vantage Specialty Chemicals MFG Chemical Tiger-Sul Actylis Zep Inc. Polymer Solutions Group Vantage Specialty Chemicals Active Minerals Advancion LCY Chemical Group Cambrex AnQore Moove PSC Group Inhance Technologies Italmatch Chemicals Solenis Seqens FXI Acquisition year 2017 2017 2018 2019 2015 2019 2013 2009 2016 2017 2019 2016 2018 2019 2018 2019 2018 2018 2019 2016 2015 2019 2019 2015 2017 2017 2016 2019 2015 2019 2017 2018 2015 2019 2019 2015 2019 2019 2018 2018 2017 2016 2017 Sector Specialties Specialties Plastics Specialties Specialties Plastics Specialties Basics Pharma/Fine Basics Specialties Pharma/Fine Specialties Pharma/Fine Specialties Specialties Diversified Specialties Specialties Specialties Specialties Pharma/Fine Basics Basics Specialties Specialties Ag/Fertilizers Specialties Specialties Specialties Specialties Specialties Specialties Basics Pharma/Fine Basics Specialties Services Specialties Specialties Specialties Specialties Specialties managing director/specialty chemicals with TM Capital (New York), an investment bank. “In the past twelve months, many sellers have not even attempted to put businesses on the market because it was a challenging year and companies were coming off depressed EBITDA. They also recognized they didn’t want to go through a sale process that could fail.” For the broader M&A market “price multiples, which tend to move inversely to interest rates, have tipped downward over the last year, but only slightly so far,” Bain said. In chemicals, “multiples have cooled down,” Covindassamy noted. Turning a corner Signs of a turnaround have emerged in the past few months. On a year-to-date basis through March 25, chemicals M&A volumes and values are up 7% and 40%, respectively, from 2023 levels, according to CW data. There are also some signs that business performance bottomed out or started to turn positive in the fourth quarter. In a survey of 50 chemical makers by CW , the average company reported adjusted earnings of about 85 cents per share, slightly ahead of analysts’ consensus estimate of about 83 cents per share, as reported by S&P capital IQ. “As we enter 2024, we expect near-term demand to remain pressured by elevated inflation, high interest rates and geopolitical tension, particularly in building and con-struction and durable goods end markets,” Dow CFO Jeffrey Tate said during the company’s fourth-quarter earnings call on Jan. 25. “That said, we are seeing some initial positive indicators.” These include relatively low inventory levels, moderating inflation and resilient US consumer spending, according to Tate. This cautious optimism has flowed through to M&A. “There is some optimism that we are at a point now where things could move,” Covindassamy said. “It’s about seller expectations and buyer willingness to pay.” “We are seeing deals … not at the speed that you saw in 2021, but you are starting to see deals get done,” said Paul Greenfield, managing director with Moelis & Co. (Washington, DC), an investment bank. “Interest rate cuts could be helpful, we’ll monitor that, but people are getting back into the business of doing deals.” Greenfield cited IFF’s sale of its pharma chemweek.com *Selected chemical producers owned by private equity that were acquired before 2020. Some investments may be minority stakes. Source: Chemical Week research; S&P Capital IQ. Data compiled March 27, 2024. © 2024 S&P Global 20 | Chemical Week | March 25–April 1, 2024

Chemical Week March 25/April 1: Page 20