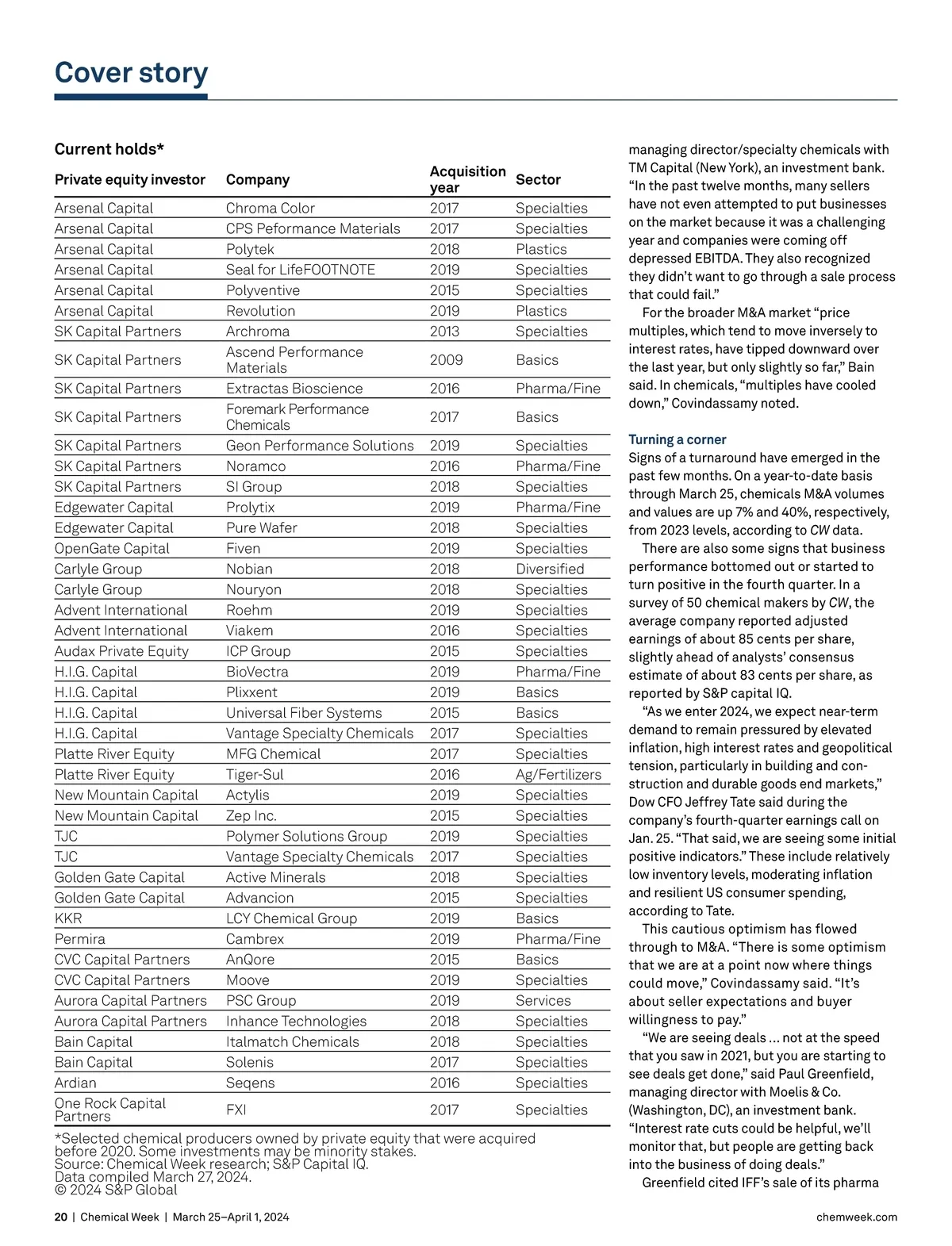

Cover story solutions business to Roquette for $2.85 billion (p. 13), which was announced on March 19. The deal had an EBITDA multiple of 13x, indicating that buyers and sellers can start to bridge gaps. “Business is improving, the pipeline is coming back, pitch activity is percolating,” Giorgio said. “These are leading indicators of a slightly better M&A market.” With inflation in the US continuing to exceed the Federal Reserve’s 2% target, expectations for interest rate cuts have shifted in recent weeks. Many M&A market participants are not expecting rate cuts until the second half of this year or later. Still, stable rates — even if relatively high — are vasty preferable to increasing rates. “There is comfort that rates are not going to go higher and will gradually come down, ‘gradual’ being the operative word,” Televan-tos said. So, while capital costs will remain high relative to the 2008–22 period, “at least we know what it is, and it’s not likely to go higher,” he added. “I think rate cuts are coming, maybe a little later than we had previously thought,” Greenfield said. “But the key thing is that we’ve been in this high-rate environment for a while now … the market is more used to it.” Despite higher rates, the window for financing is open. “Debt availability is up [compared with last year], but not what it was at the peak,” Televantos said. “The cost is higher, but you can plan for that.” For most borrowers, “the window is open,” said Thomas Watters, managing director at S&P Global Ratings. For investment-grade companies, capital market access was never really a problem, but for speculative-grade issuers, “it could be dicey and with higher rates,” he added. “They’ve had higher interest expenses, so have had to solve for that.” The gulf in valuation expectations between buyers and sellers is starting to narrow, although buyers have moderated their expectations first, bankers said. “Buyers have realized that this is the rate environ-ment, they’ll price that in and the real movement now to open up M&A is that sellers need to move a little closer to where buyers are,” Greenfield said. “I think you see that in some of the deals that have gotten done in the past few months.” Sellers may still have to adjust expecta-tions, according to Ryan Meany, managing partner with Edgewater Capital Partners (Cleveland), a private equity firm. “We have chemweek.com not seen bid-ask spreads narrow a signifi-cant amount just yet,” he said. “I think they should, that would be part of the outcome of the higher cost of capital … its mainly due to sellers, expectations are still a bit elevated in the current environment.” Acceptance of a new normal is gradually taking hold, according to Giorgio. “Sellers are reluctantly accepting that this is the new pricing dynamic,” he said. “And there’s a recognition that 2022 [valuations] were Even if interest rates remain relatively high, stabilization is good for M&A. abnormally high. Unsustainable EBITDA for many businesses and very fulsome multiples combined to create a very robust environ-ment a couple of years ago, which set expectations for sellers that were unrealistic.” Valuations are settling for nonpremium assets, according to Greenfield. “Our view is that premium assets will still go for premium multiples,” he said. “But in chemicals, you see a divergence between premium assets and the next tier down … you will see lower valuations for the next tier down. It shows things are getting more back to normal,” compared to the inflated environment of the immediate post-pandemic era, he added. Difficult exits One consequence of a weak M&A market in 2023 — and the roller coaster ride that has been seen this decade — is that private equity firms have held onto many assets for longer than a typical hold period of five years or so. A survey by CW found over 40 chemi-cals assets acquired by private equity in 2019 or earlier that are still held by those same private equity investors (table; note that some of these assets are minority invest-ments). Average hold periods for private equity “have ticked up to six-plus years,” compared with about five years historically, Daniel Bruck, principal/industrial growth with Arsenal Capital, said during the CM&E Group early-March webinar. Some private equity firms, such as SK Capital Partners (New York), may adopt a holding-company-like strategy for invest-ments, and have historically been comfortable with longer hold periods. But most do not operate this way, and many firms are facing pressure from investors to unload assets that have been held for several years or more. “Exit activity fared even worse than dealmaking in 2023, as rising interest rates and macro uncertainty left buyers and sellers at odds over valuations,” Bain said in its report on private equity. “Buyout-backed exits came in at $345 billion globally, a 44% decline from 2022.” Difficulty selling assets can even redound to fundraising, as private equity needs to sell assets to show investors a return and attract the next pool of capital. “The exit conundrum has emerged as the most pressing problem, as [limited partners] starved for distributions pull back new [capital] allocations from all but the largest, most reliable funds,” Bain said. “Today you have a lot of private equity firms that have not been very active for the past 18 months, and they have investors and returns they need to hit and money they need to put to work,” Greenfield said. Bain estimates total “dry powder,” or capital to invest, was about $1.2 trillion for the whole private equity industry at the end of 2023. “We have businesses that are of a vintage where we need to consider a sale,” Arsenal Capital’s Televantos noted. In February, the firm announced the sale of Seal for Life Industries LLC, a protective coatings maker that Arsenal acquired in 2019, to Henkel, in what will likely be the first of multiple exits. “Several more [sales] are in the works,” Televantos said. “We feel the performance of these businesses is strong enough to get an adequate return, so we are preparing to take them to market. Many other [private equity] firms are doing the same, so we are seeing a significant increase in deal flow.” CW ’s survey found six chemical businesses owned by Arsenal that were acquired in 2019 or earlier. Some other businesses were acquired in the early 2020s. However, while there are clear pressures to exit for many private equity firms, and many such deals are in the pipeline, this pressure has yet to translate into a spate of announced transactions. Just three chemicals M&A transactions announced so far in 2024 involved a private equity seller, including Arsenal’s sale of Seal for Life, according to CW data, compared with 14 deals that involved private equity on the buy side. March 25–April 1, 2024 | Chemical Week | 21

Chemical Week March 25/April 1: Page 21